Here is a wrap up of the some of the issues PalmTrack covered in April 2022:

Indonesia’s palm oil export ban: Indonesia has recently banned the export of palm oil. The ban encompasses several products—CPO, PAO, POME, RBDPL, RBDPL, RBDPO, and UCO—coming to a total of 12 HS codes. We turned to several sources following news of three executives of key palm companies and a senior bureaucrat charged in connection to the country’s cooking oil crisis that occurred just ahead of the ban, with one stating that “[t]he image of the industry is bad. If it is true, it has to be proved in court, but it is as if the whole industry is guilty.”

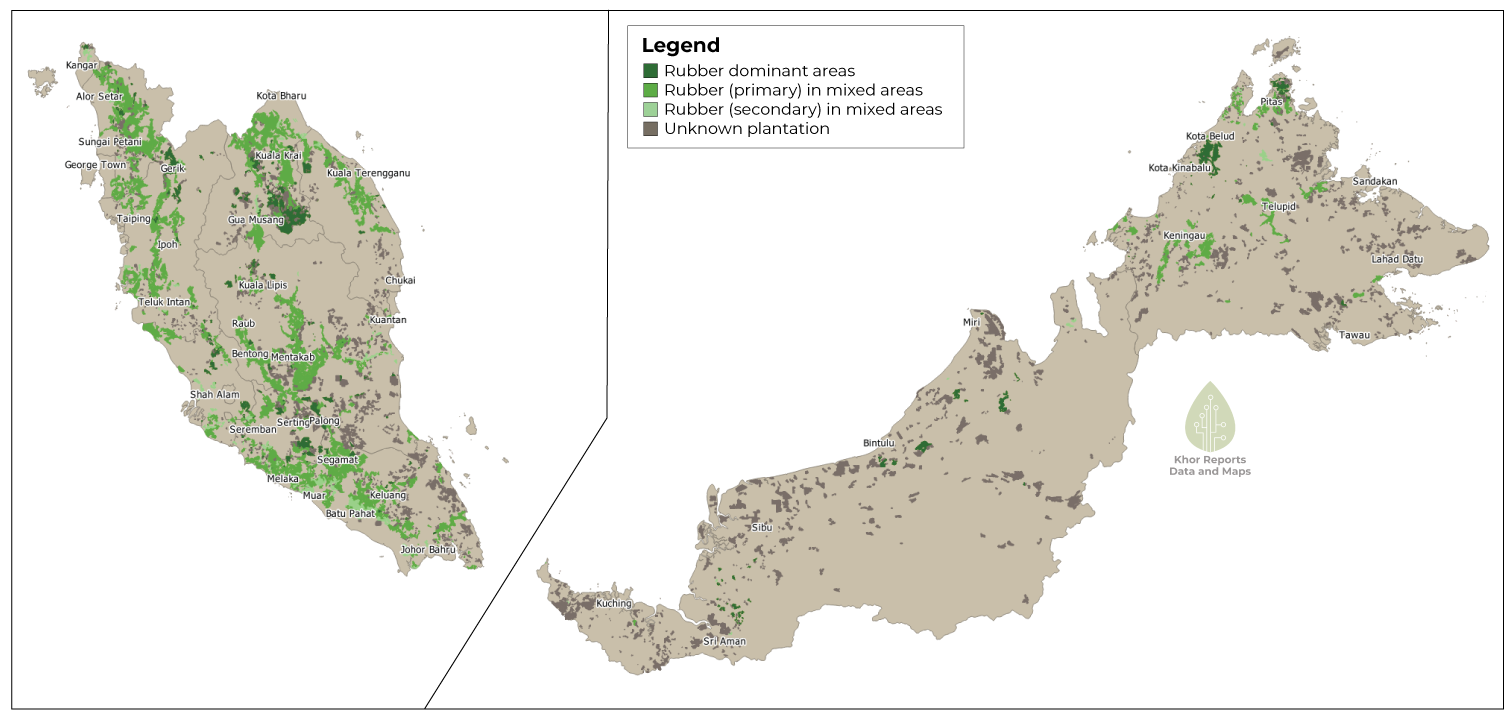

Palm’s Animal Feed Hopes: Biomass from oil palm trees have important uses, but current uses are not always considered optimal by the palm industry. Key applications include empty fruit bunch (EFB) and fronds as mulch in plantations, liquid waste for biogas, PKM as mixture for fodder (for ruminants - cows) and other wastes for fertilizers. PalmTrack has published two posts on this—one on feed for dairy cattle, and the other on chicken feed.

Weather and rainfall: On notable rainfall events (30 days to 11 Apr 2022), 30 days accumulated rainfall was est. above 300mm all across most of Borneo, South & Southeast Sulawesi, and smaller areas of central Peninsular Malaysia. The Australian BOM issued a weather project on 12 Apr 2022, with predictions that La Niña is expected to eventually return to neutral in the southern hemisphere in autumn or early winter.

Tankers from Indonesia: Port calls for 28 Mar–13 Apr 2022 (14 days) count, c.60 palm-related tankers, with sample net tonnage c.330k (versus nearly two months ago, 14 days to 13 Mar, c.60 tankers with sample net tonnage c.297k). These two weeks (28 Mar–13 Apr), the share of port calls was higher for ASEAN (other than Malaysia and Singapore), CIS, and South Asian ports (versus 14 days to 13 Mar).

Prices, projections, and policy jitters: Many in the palm oil world are familiar with the three Gurus of palm oil outlook: Fry (my ex-boss), Mielke, and Dorab. We covered their views (and that of others) from the big KL Price Outlook Conference (POC) 2022 powwow.

Khor Reports’ PalmTrack is an independent research service that tracks palm tanker movements and reports trade of palm products (and shipments, upon request) for selected trade routes. It features a forward-looking market topic and sharp analysis every quarter, e.g. palm biofuels issues & opportunities for Jan–Mar 2022. Subscribe now!